Why Contractors Sell Their Business: A Practical Exit Guide

Selling a contracting business, formally known as a business exit or ownership transition, is driven primarily by retirement needs and succession gaps rather than pure financial opportunism. The construction industry’s survival rate tells part of the story: only 36% of construction firms survived the period from 2011 to 2022. That statistic reflects an industry where owners carry enormous personal risk for decades, and eventually, most reach a point where selling is the clearest path forward. Whether you are approaching retirement, burning out, or facing cash flow pressure, understanding why contractors sell their business gives you the clarity to act on your own terms.

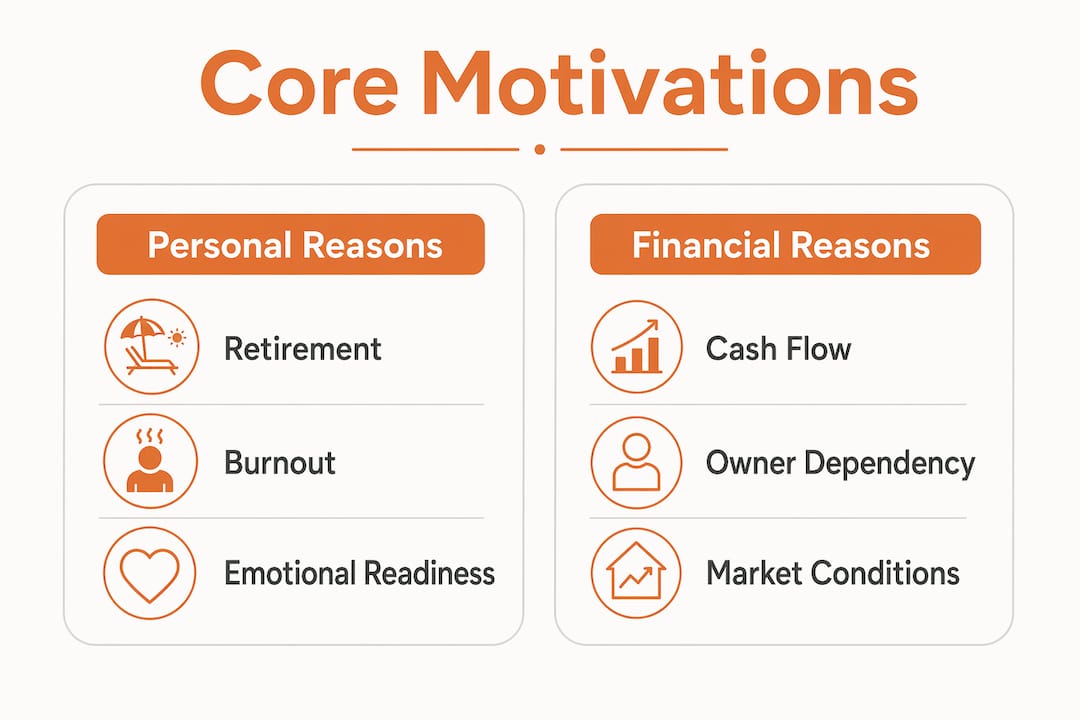

Why contractors sell their business: the core motivations

The top reasons contractors exit fall into two categories: personal and financial. Personal reasons dominate. Retirement without a ready successor is the single most common trigger. Many contractors built their companies around their own relationships, licenses, and judgment. When they look around and see no family member or key employee prepared to take over, selling to an outside buyer becomes the only viable path.

Burnout ranks close behind retirement as a personal driver. Construction is physically demanding, legally complex, and operationally relentless. Owners manage crews, chase payments, handle OSHA compliance, and absorb project risk simultaneously. After 20 or 30 years, that weight accumulates. Many owners reach a point where the business no longer energizes them, and continuing feels like a liability rather than an asset.

Financial pressure also pushes contractors toward a sale. 82% of failed businesses cited cash flow problems as a contributing factor. Slow payment cycles from general contractors or owners create chronic stress, and when a business depends entirely on the owner to keep cash moving, that stress has no exit valve except the owner’s own exit.

What personal factors motivate contractors to sell?

Personal motivations are rarely simple. They combine retirement timing, family dynamics, health, and identity in ways that make the decision feel both urgent and complicated.

The most common personal factors include:

- Retirement without succession. When no family member or project manager with 3+ years of operational experience is ready to take over, owners sell rather than risk a disorderly handoff.

- Physical burnout. Decades of field exposure, safety liability, and 60-hour weeks take a measurable toll. Many contractors in their late 50s find the physical demands no longer match their capacity.

- Lifestyle change. Some owners want to travel, spend time with family, or pursue other interests while they are still healthy enough to enjoy them.

- Legacy and timing. Selling while the business is profitable preserves the owner’s reputation and protects employees. Waiting too long risks a distressed sale at a fraction of fair value.

The emotional dimension of selling is real and often underestimated. Many contractors built their company from nothing, and the business carries their name, literally in some cases. Separating personal identity from business value is one of the hardest parts of the exit process.

Pro Tip: Start conversations with a business broker or M&A advisor at least two years before you plan to sell. Early engagement gives you time to address valuation gaps without pressure.

Contractors who recognize the difference between systemic business problems and personal readiness make better exit decisions. Operational fixes sometimes resolve the underlying issue without requiring a sale. If the business runs well but you are personally done, that is a clear signal to sell. If the business has structural problems, fix them first or price accordingly.

How do financial and operational risks influence the decision to sell?

Financial risk is the most concrete factor buyers examine, and it directly affects what they will pay. Owner-dependent businesses receive significantly lower offers than those with documented systems and capable management teams.

Businesses with formal management teams trade at 5–7x EBITDA, while owner-dependent operations typically receive only 2.5–4x EBITDA. That gap represents hundreds of thousands of dollars on a mid-sized contracting business. Buyers discount heavily when they see that the owner is the business.

The financial risks that most often reduce offers include:

- Undocumented systems. When processes exist only in the owner’s head, buyers see transition risk and price it in.

- Customer concentration. A business where one client represents 40% or more of revenue is a red flag. Buyers fear losing that client post-sale.

- Poor financial records. Mixed personal and business expenses, inconsistent bookkeeping, and missing CPA-reviewed statements all erode buyer confidence.

- Slow payment cycles. Chronic accounts receivable delays signal operational weakness and reduce working capital projections.

Subcontractor dependency creates a parallel risk. When a business relies on a small pool of subcontractors without formal qualification processes, buyers see execution risk. Resolving these dependencies before going to market strengthens your position.

Pro Tip: Ask your CPA to prepare three years of reviewed financial statements before listing. Buyers trust audited or reviewed numbers far more than owner-prepared spreadsheets.

Preparation over 24–36 months, including clean books, documented SOPs, a capable management team, and reduced owner involvement, increases sale value significantly. That timeline is not arbitrary. It takes time to build buyer confidence into the business itself, not just the pitch.

What operational and legal complexities affect selling a contracting business?

Construction business sales involve legal and operational layers that most other industries do not face. Buyers and their advisors know this, and they scrutinize these areas closely.

The four most critical areas are:

- Contractor license transferability. Most state contractor licenses are tied to a qualifying individual, not the business entity. A change of ownership may require the buyer to obtain a new license or designate a new qualifier, which can delay or derail a deal.

- Surety bond transfer. Surety bonds are often tied to the owner’s personal credit and financial history. Bonds frequently require re-approval after an ownership change, which can interrupt active projects. Contractors should obtain written statements from their surety company at least 12 months before a planned sale.

- Contract backlog and revenue predictability. Buyers pay for future revenue, not just historical performance. A strong backlog of signed contracts with creditworthy clients increases sale price. A thin or uncertain backlog reduces it.

- Due diligence intensity. Construction due diligence averages 250–300 hours, covering equipment audits, forensic contract reviews, insurance verification, and license checks. That process typically runs 45–90 days and requires the seller to be organized and responsive.

| Complexity Area | Buyer Concern | Recommended Action |

|---|---|---|

| Contractor license | Continuity of operations | Identify a qualified successor or buyer qualifier early |

| Surety bonding | Project completion risk | Get surety written statement 12+ months pre-sale |

| Contract backlog | Revenue predictability | Maintain signed contracts with clear terms |

| Financial records | Accuracy and trust | CPA-reviewed statements for 3 prior years |

| Equipment condition | Asset value and liability | Conduct independent equipment appraisal |

Pro Tip: Engage a construction-specific M&A attorney, not a general business attorney. The nuances of contractor licensing and surety transfer require specialized knowledge.

Understanding construction management service structures also helps sellers frame their business’s value to buyers who may be evaluating multiple acquisition targets in the sector.

How can contractors prepare their business to improve sale value?

Preparation is the single most controllable factor in a contractor’s exit outcome. Preparation 12–18 months before sale can increase proceeds by 20–40%. That is a material return on the time invested.

The most effective preparation steps are:

- Document your SOPs. Write down every repeatable process: estimating, scheduling, procurement, safety protocols, and billing. Documented workflows reduce perceived transition risk and add 0.5–1.0 turns to your EBITDA multiple.

- Build a management team. A superintendent, project manager, and office manager who can run operations without you makes the business transferable. Buyers pay for businesses that do not require the seller to stay.

- Qualify your subcontractors. Resolve subcontractor qualification gaps before going to market. Buyers conducting due diligence will find them, and unresolved issues become negotiating leverage against you.

- Clean your financials. Separate all personal expenses from business accounts. Maintain CPA-reviewed profit and loss statements. Buyers trust clean numbers and discount businesses where cleanup is required.

- Engage your surety company early. Confirm bond transfer conditions in writing. Surprises in this area kill deals at the worst possible moment.

The goal of preparation is to make your business look like it runs itself. That is the version buyers pay a premium for.

Key takeaways

Contractors who sell on their own terms do so because they prepared early, documented their operations, and addressed financial and legal risks before going to market.

| Point | Details |

|---|---|

| Retirement drives most sales | Succession gaps and lack of a ready successor are the top reasons contractors exit. |

| Owner dependency lowers value | Businesses without management teams receive 2.5–4x EBITDA versus 5–7x for those with formal teams. |

| Surety bonds require early action | Get written bond transfer conditions from your surety company at least 12 months before sale. |

| Preparation increases proceeds | Starting 12–18 months early can raise sale proceeds by 20–40% through documentation and financial cleanup. |

| Due diligence is intensive | Construction deals average 250–300 hours of buyer review, requiring sellers to be organized and responsive. |

What I’ve learned about when contractors should actually sell

After years of working inside the AEC industry, I have seen contractors make two consistent mistakes. The first is waiting too long. They hold on past the point where the business is growing, past the point where they have energy to prepare, and into a period where the sale becomes distressed. The second mistake is selling too fast, without preparation, and leaving significant value on the table.

The contractors who exit well share one trait: they got outside advice early. Not from their accountant alone, and not from a friend who sold a different kind of business. They worked with advisors who understood construction-specific valuation, surety bonding, and license transfer. That specialized knowledge changes the outcome.

The emotional barrier is real. Selling feels like admitting the chapter is over. But the contractors I respect most reframe it differently. They see the sale as the final project, the one where their decades of discipline and relationship-building get converted into lasting financial security. That reframe makes the preparation feel worth it.

If your business depends entirely on you to function, fix that before you list. Not because buyers demand it, but because you deserve to sell something that reflects what you actually built.

— Rowena

Building the team that makes your business worth buying

Contractors preparing for an exit often discover that their biggest valuation gap is not financial. It is the absence of a capable, documented management team. Buyers want to acquire a business, not a job.

Constructconnect-rconstructionsolutions specializes in recruiting and sourcing for the AEC industry, with 30+ years of experience placing pre-vetted superintendents, project managers, and operations leaders in contracting firms. If you are preparing for a sale or restructuring your business to reduce owner dependency, building the right team now directly increases what a buyer will pay. Explore AEC recruiting services to find the management talent that makes your business transferable and your exit terms stronger.

FAQ

Why do most contractors decide to sell their business?

Retirement and succession gaps are the top drivers. When no family member or key employee is ready to take over, selling to an outside buyer becomes the most practical path.

How long does it take to sell a contracting business?

Most construction business sales take 12–24 months from preparation to close. Due diligence alone typically runs 45–90 days, requiring organized financial and legal records.

What reduces the sale price of a contracting business?

Owner dependency, undocumented systems, customer concentration, and poor financial records are the most common reasons buyers discount their offers.

What is EBITDA and why does it matter for contractors selling?

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It is the standard measure buyers use to value contracting businesses, with multiples ranging from 2.5x to 7x depending on management depth and operational documentation.

When should a contractor start preparing to sell?

Start at least 24–36 months before your target sale date. That window gives you time to clean financials, build a management team, document SOPs, and resolve surety and licensing issues without pressure.