Small Contractor Classification: What Contractors Need to Know

Small contractor classification is the official designation that determines whether a contractor meets the size and revenue thresholds set by the IRS and the SBA for tax treatment and federal contracting eligibility. Two separate regulatory frameworks govern this status, and confusing them is one of the most common compliance mistakes contractors make. The IRS applies its definition under IRC §460 for tax accounting purposes, while the SBA uses NAICS code-based size standards to determine eligibility for federal set-aside contracts. Knowing which framework applies to your situation, and when, directly affects your tax filing choices, your ability to bid on government work, and your long-term growth strategy.

What is small contractor classification under IRS rules?

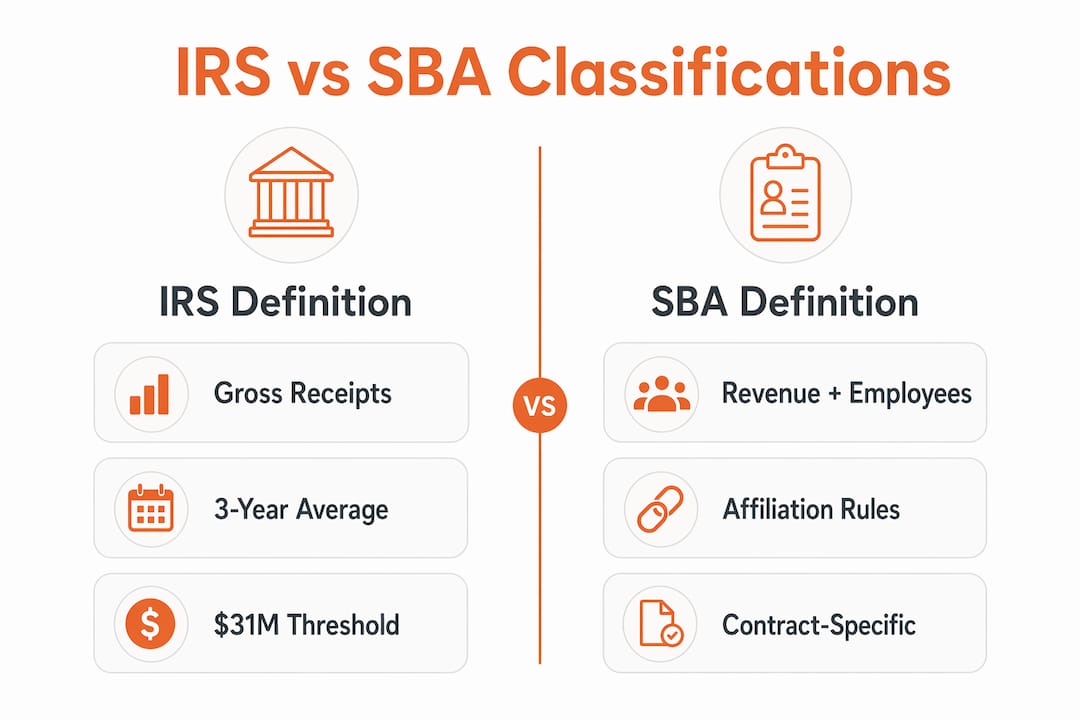

The IRS defines a small contractor under IRC §460 using two tests: annual gross receipts and estimated contract duration. A contractor qualifies when average annual gross receipts for the prior three tax years fall below the inflation-adjusted threshold, and when the contract is reasonably expected to be completed within two years. For 2025, that gross receipts threshold sits at approximately $31 million. That number adjusts each year for inflation, so you need to verify the current figure with your tax advisor before filing.

This classification matters because it unlocks favorable accounting methods. Qualifying small contractors can elect the completed contract method (CCM) or the cash method, both of which allow income recognition to be deferred until a project closes. For contractors managing multi-year projects, that deferral can produce meaningful cash flow advantages and reduce tax liability in high-revenue years.

The two-year contract rule is often overlooked. A contractor might clear the revenue threshold but still fail the IRS test if the contract is structured to run longer than two years. Both conditions must be satisfied simultaneously.

- Annual gross receipts must average below $31 million over the prior three tax years

- The contract must be estimated to complete within two years from the start date

- Both tests apply at the time the contract is entered, not at completion

- Exceeding the threshold in a single year does not automatically disqualify you if the three-year average remains below the limit

- Electing the completed contract method requires formal documentation and consistent application

Pro Tip: Review your three-year average gross receipts every year before bidding on new long-term contracts. A single high-revenue year can push your average above the IRS threshold and eliminate your accounting method options for contracts signed that year.

How does the SBA define small contractor status for federal contracting?

The SBA’s definition of a small contractor operates entirely separately from the IRS framework. The SBA assigns size standards by NAICS code, the North American Industry Classification System, and those standards vary significantly by trade. SBA size standards for construction range from $19 million in average annual revenue for specialty trade contractors to $47 million for commercial builders, with some categories measured by employee count instead of revenue.

The SBA calculates revenue using a three-year average, similar to the IRS, but the comparison stops there. The SBA also counts employees across a rolling 12-month period, and for employee-based categories, thresholds typically fall between 500 and 1,500 workers. Specialty trade contractors generally face a $19 million revenue cap, while general commercial building contractors can qualify at up to $45 million as of 2026.

| Construction Category | Size Standard Type | Typical Threshold (2026) |

|---|---|---|

| Specialty trade contractors | Revenue | $19 million (3-year average) |

| Commercial building contractors | Revenue | $45 million (3-year average) |

| Heavy and civil engineering | Revenue | $47 million (3-year average) |

| Some engineering subsets | Employee count | 500–1,500 employees |

Affiliation rules add another layer of complexity. The SBA requires that you include the revenues and employees of any affiliated companies when calculating your size. Affiliation can arise from common ownership, shared management, or contractual relationships. A contractor who appears small on paper may exceed the threshold once affiliates are counted in.

To qualify for federal set-aside contracts, a business must also be for-profit and independently owned, not dominant in its field nationally, and fully compliant with SBA affiliation rules. These qualitative criteria exist alongside the numerical thresholds, and failing any one of them removes eligibility regardless of revenue size.

What nuances differentiate IRS and SBA small contractor classifications?

The IRS and SBA classifications share the word “small” but measure entirely different things. Tax and SBA definitions differ in their purpose, their thresholds, and their consequences. Passing the IRS test gives you accounting method flexibility. Passing the SBA test gives you access to set-aside contracts. Passing one does not guarantee the other.

A contractor with $28 million in annual gross receipts qualifies as small under the IRS definition for 2025. That same contractor may or may not qualify under the SBA, depending on which NAICS code governs the specific contract being bid. Eligibility is contract-specific under SBA rules, meaning your business can be “small” for one solicitation and “other than small” for another, depending on the NAICS code assigned to each contract.

State-level classification adds a third layer. Many states apply their own contractor licensing categories based on revenue, bonding capacity, or employee count. Some states use the “ABC test” to determine whether workers are properly classified as independent contractors rather than employees. Misclassifying workers under state law carries penalties that are separate from any federal compliance issues.

Key distinctions contractors must track:

- IRS classification applies at the time a contract is signed; SBA classification applies at the time of offer submission

- IRS uses a single gross receipts threshold; SBA uses NAICS-specific thresholds that vary by trade

- SBA affiliation rules can disqualify a contractor even when standalone revenue falls below the threshold

- The IRS small contractor test does not guarantee SBA small business program qualification

- State licensing boards may impose separate size or capacity requirements unrelated to either federal standard

Understanding subcontractor dependency in your firm also affects how affiliation rules apply, particularly when subcontractors share ownership or management with your company.

What are practical steps to manage your small contractor status?

Managing small contractor classification requires active monitoring, not a one-time check. The most common mistake contractors make is assuming their status is fixed. Revenue grows, affiliates change, and NAICS codes shift across different solicitations.

-

Verify the NAICS code on every solicitation before submitting an offer. The assigned code determines which SBA size standard applies. A single contract can fall under multiple possible codes, and the contracting officer’s choice controls your eligibility for that bid.

-

Calculate your three-year average revenue annually. Both the IRS and SBA use multi-year averages, so a single strong year does not immediately disqualify you. Track the trend and project forward so you are not surprised at bid time.

-

Audit your affiliates before each certification cycle. SBA affiliation rules are strict and frequently misunderstood. Include any company where common ownership or shared management exists, even informally.

-

Know the SBA appeal window. If a contracting officer challenges your small business status, you have 15 calendar days from notification to file an appeal with the SBA Office of Hearings and Appeals. Missing that deadline forfeits your appeal rights entirely.

-

Pivot NAICS codes strategically as you grow. Contractors exceeding size standards for their primary NAICS code often bid on contracts under other codes with higher thresholds to maintain small business eligibility while they scale.

-

Elect accounting methods proactively. Once you confirm IRS small contractor status, work with a CPA to elect the completed contract method or cash method before the tax year closes. Retroactive elections are rarely permitted.

Pro Tip: Use construction software tools that track revenue by project and NAICS category. Keeping that data organized makes annual size recertification and IRS threshold calculations significantly faster and more accurate.

Understanding multi-skilled workforce strategies also helps small contractors stay competitive without inflating headcount in ways that could affect SBA employee-based thresholds.

Key Takeaways

Small contractor classification requires separate compliance with IRS gross receipts rules under IRC §460 and SBA NAICS-based size standards, and meeting one does not satisfy the other.

| Point | Details |

|---|---|

| IRS threshold for 2025 | Average gross receipts below $31 million over three years, with contracts expected to complete within two years. |

| SBA standards vary by trade | Thresholds range from $19 million for specialty trades to $47 million for heavy construction, based on NAICS code. |

| Classifications are independent | Qualifying under IRS rules does not guarantee SBA small business status; both require separate verification. |

| Appeal window is strict | SBA size challenges must be appealed within 15 calendar days or the right to appeal is permanently lost. |

| NAICS code controls eligibility | Your small business status is contract-specific; the same firm can qualify as small on one bid and not another. |

Why I think most contractors underestimate this classification

Most contractors treat small business classification as a checkbox. They confirm their revenue is below a threshold, register in SAM.gov, and move on. That approach works until it doesn’t, and when it fails, it usually fails at the worst possible moment: during a bid protest or a tax audit.

What I’ve seen repeatedly is that contractors focus entirely on the SBA side because that’s where the contracting opportunity is visible. The IRS classification gets ignored until a CPA raises it at year-end, often too late to elect the most favorable accounting method. The completed contract method, in particular, can defer a significant tax liability on a large project, but you have to elect it before the tax year ends.

The affiliation rules are where I see the most damage. A contractor who co-owns a material supply company with a family member may not realize that company’s revenue counts toward their SBA size calculation. By the time a contracting officer flags it, the contract is already at risk.

My advice is to treat classification as a quarterly review item, not an annual one. Revenue trends, new affiliates, and NAICS code changes on solicitations all move faster than most contractors expect. The contractors who stay ahead of this are the ones who build classification monitoring into their standard business operations, not their crisis response.

— Rowena

How Constructconnect-rconstructionsolutions supports small contractors

Small contractors who understand their classification still need the right people and partners to execute on the opportunities that classification unlocks.

Constructconnect-rconstructionsolutions brings 30-plus years of AEC industry experience to recruiting and sourcing for contractors at every stage of growth. Whether you need pre-vetted subcontractors to staff a newly won federal set-aside contract or qualified field talent to keep your headcount compliant with SBA employee thresholds, the team connects you with the right resources. The business opportunity sourcing service helps small contractors identify and qualify for projects that match their classification and capacity. For firms ready to build their bench, AEC recruiting services deliver candidates who are screened for the specific roles and certifications your projects require.

FAQ

What is the IRS revenue threshold for small contractor status in 2025?

The IRS sets the small contractor threshold at approximately $31 million in average annual gross receipts over the prior three tax years, adjusted annually for inflation under IRC §460.

Does qualifying as a small contractor under the IRS also qualify me with the SBA?

No. The IRS and SBA use separate tests with different thresholds and purposes. You must verify compliance with each framework independently.

How long do I have to appeal an SBA size determination?

You have 15 calendar days from the date of notification to file an appeal with the SBA Office of Hearings and Appeals. Missing that deadline eliminates your right to appeal.

Can my business be small for one federal contract but not another?

Yes. SBA eligibility is contract-specific and tied to the NAICS code assigned in each solicitation. The same business can qualify as small under one code and exceed the threshold under another.

What accounting methods does IRS small contractor status unlock?

Contractors who meet the IRC §460 small contractor definition can elect the completed contract method or the cash method, both of which allow income deferral until project completion.