Why Contractors Need Performance Bonds: 2026 Guide

A performance bond is a financial guarantee that a contractor will complete a project according to the terms of the signed contract. Without one, project owners carry the full financial risk of contractor default. That risk is not theoretical. Construction defaults disrupt timelines, drain budgets, and expose every party to costly legal disputes. Understanding why contractors need performance bonds is the first step toward protecting your business, winning better projects, and building a reputation that opens doors in the AEC industry.

Why contractors need performance bonds: the core case

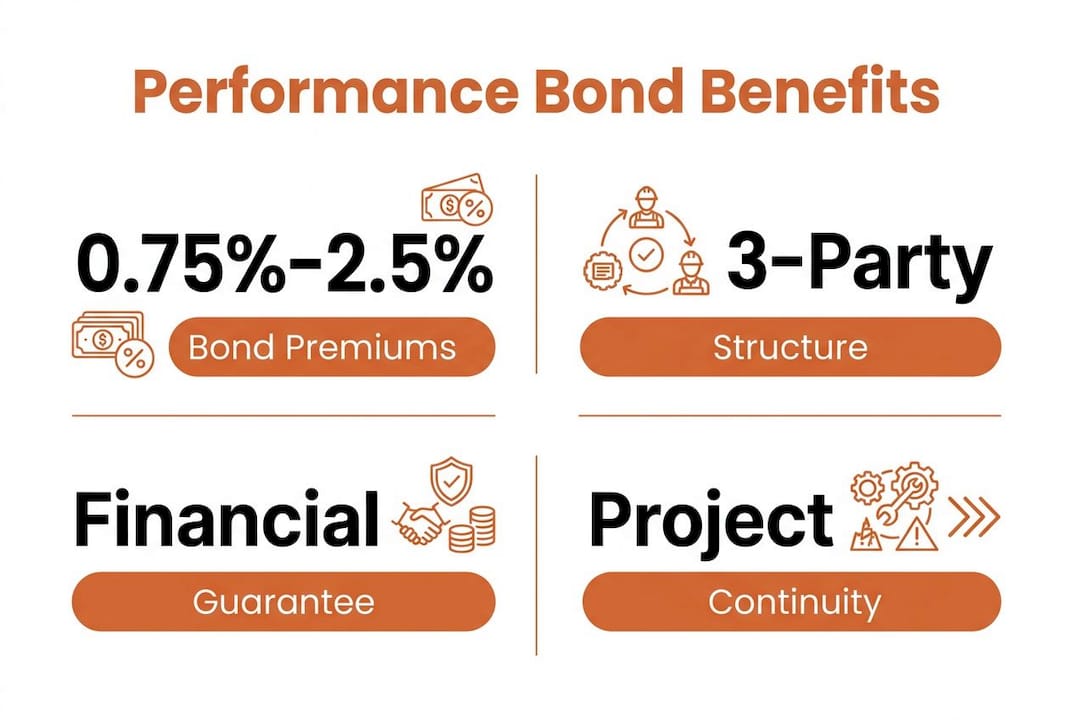

Performance bonds exist within a three-party structure: the contractor (principal), the surety company (guarantor), and the project owner (obligee). The surety company underwrites the bond after evaluating the contractor’s financial health, project history, and capacity. If the contractor defaults, the surety steps in to finance project completion, hire a replacement contractor, or pay the owner up to the bond’s face value.

Two major bond types appear in commercial construction. Conditional performance bonds require the owner to prove contractor default before the surety acts. On-demand bonds allow the owner to call the bond without proving fault first. Most U.S. commercial projects use conditional bonds, which give contractors more procedural protection.

Performance bonds almost always pair with payment bonds. Payment bonds guarantee that subcontractors and suppliers get paid even if the general contractor fails. Together, they form the standard bonding package on most public and large commercial projects.

Pro Tip: Always confirm whether a project requires both a performance bond and a payment bond before submitting your bid. Assuming one covers the other is a costly mistake.

Benefits for contractors: why bonding strengthens your business

Bonding is not just a legal checkbox. It is a direct signal to project owners that your company has the financial stability and track record to deliver. Contractors with bonds aligned to AIA A312 standards show improved bid success by giving owners clearly defined risk management from day one.

The business advantages of holding a performance bond are concrete:

- Competitive bid positioning. Bonded contractors qualify for a wider range of public and commercial projects. Owners shortlist bonded firms first because the bond reduces their exposure.

- Shared financial risk. The surety absorbs a portion of the financial risk if a project goes sideways. That protection limits your company’s direct financial exposure on large contracts.

- Credibility with lenders and investors. Banks and equity partners treat bonding capacity as a proxy for financial discipline. A strong bonding history supports better financing terms.

- Reputation as a reliable partner. Owners and general contractors remember which subcontractors and GCs carry bonds. That reputation compounds over time into repeat business and referrals.

- Access to higher-value projects. Commercial projects above $3M routinely require performance and payment bonds as a baseline condition of bidding.

Bond premiums on commercial work typically range from 0.75% to 2.5% of the contract price. That cost is real, but it is far smaller than the financial and reputational damage of a disputed default.

Pro Tip: Build your bonding capacity before you need it. Sureties reward contractors who maintain clean financials and a documented project history, not those who apply in a rush before a bid deadline.

Legal and industry requirements for performance bonds in 2026

Federal law sets the floor for bonding requirements. The Miller Act mandates performance and payment bonds on all federal construction contracts exceeding $100,000. Every state has its own version, commonly called a “Little Miller Act,” which applies the same logic to state-funded public works. Thresholds vary by state, so you need to verify local requirements before bidding on any public project.

Commercial bonding thresholds follow market norms rather than statute. The table below summarizes the key benchmarks contractors encounter in 2026.

| Requirement | Threshold or Standard |

|---|---|

| Miller Act (federal public works) | Contracts over $100,000 |

| State Little Miller Acts | Varies by state; often $25,000–$100,000 |

| Commercial GC standard | Projects above $3M typically require bonds |

| Typical bond value | 10% of the contract sum in many commercial settings |

| Bond premium range | 0.75%–2.5% of contract price |

Surety company licensing matters as much as the bond itself. The U.S. Treasury publishes an annual list of approved sureties (Circular 570) for federal projects. Owners on private projects also check surety credit ratings through agencies like A.M. Best. A bond from an unlicensed or low-rated surety can be rejected outright, disqualifying your bid after the fact.

For contractors building their bonding qualification profile, the surety’s underwriting criteria are the practical starting point. Sureties evaluate working capital, net worth, backlog, and the size of projects you have completed. Your bonding limit reflects what the surety believes you can handle without defaulting.

Common pitfalls contractors face with performance bonds

Misunderstanding bonding mechanics costs contractors real money and real opportunities. The most common errors are preventable with the right preparation.

- Confusing bid bonds with final bonds. A bid bond guarantees you will enter the contract if selected. It does not guarantee the surety will issue a performance or payment bond at contract award. Final bonds go through separate underwriting. Winning a bid and then failing to secure the final bond is a serious breach.

- Weak financial documentation. Sureties require audited or reviewed financial statements, proof of working capital, and a track record of completed projects near the requested bond size. New or fast-growing contractors often face lower bonding limits or higher premiums until their financials mature.

- Misaligned bond wording. A performance bond must align with the specific milestones and obligations in the construction contract. Without that alignment, the bond provides little practical protection for either party. The value of a bond depends heavily on the clarity and claimability of its wording.

- Treating bonds as a substitute for project controls. Bonds provide financial backing. They do not replace strong scheduling, subcontractor management, or quality oversight. Contractors who rely on the bond as a safety net instead of managing projects well tend to exhaust their bonding capacity quickly.

- Ignoring capacity limits. Your bonding capacity is finite. Taking on too many bonded projects simultaneously can push you past your aggregate limit, blocking new opportunities at exactly the wrong moment.

Understanding subcontractor performance bonds adds another layer of protection on large projects where GCs carry risk for their entire supply chain.

How performance bonds protect project owners and ensure continuity

From the owner’s perspective, a performance bond converts contractor default from a legal crisis into a financial remedy. Bonds give owners access to funds if a contractor defaults, avoiding slow and uncertain legal proceedings. That speed matters enormously on projects with hard completion deadlines.

The surety’s role in a claim scenario is active, not passive. The surety investigates the default, then chooses from several remedies: financing the original contractor to complete the work, hiring a replacement contractor, or paying the owner up to the bond amount. That pre-arranged structure is what separates bonded projects from unbonded ones when things go wrong.

| Scenario | Without a bond | With a performance bond |

|---|---|---|

| Contractor defaults mid-project | Owner pursues litigation; project stalls | Surety funds completion or replaces contractor |

| Subcontractors unpaid | Liens filed against property | Payment bond covers subcontractor claims |

| Owner’s financial exposure | Unlimited; depends on legal outcome | Capped at bond value |

| Project timeline impact | Months of delay typical | Surety-managed transition minimizes delay |

Bonds do not prevent defaults. They provide a pre-arranged financial remedy that caps losses and enables rapid replacement to avoid project shutdowns. That distinction matters for contractors too. Carrying a bond signals to owners that you have already accepted accountability for project delivery, which is a powerful differentiator in competitive bids.

Contractors who want to reduce subcontractor unreliability risks should treat bonding as one part of a broader risk management approach, not the whole solution.

Key Takeaways

Performance bonds are the most direct tool contractors have to prove financial accountability, access higher-value projects, and share risk with a surety company.

| Point | Details |

|---|---|

| Legal baseline | The Miller Act requires bonds on federal contracts over $100,000; state Little Miller Acts extend this to public works. |

| Bond cost | Premiums run 0.75%–2.5% of contract price, a small cost relative to the risk they offset. |

| Bid bonds vs. final bonds | A bid bond does not guarantee a final performance bond; each requires separate underwriting. |

| Bonding capacity | Sureties set limits based on audited financials and project history; build capacity before you need it. |

| Owner protection | Bonds give owners a pre-arranged remedy on default, capping financial exposure and reducing project delays. |

Why I think contractors underestimate bonding until it’s too late

After years of working in the AEC industry, I have watched contractors lose major project opportunities not because they lacked skill, but because they had not built their bonding capacity in advance. Bonding is treated as an afterthought until a bid requirement forces the issue. By then, it is too late to fix weak financials or a thin project history.

The contractors I have seen succeed consistently treat their surety relationship the way they treat their bank relationship. They maintain clean, audited financials. They communicate proactively with their surety agent when project conditions change. They do not overextend their aggregate bonding limit chasing volume. That discipline compounds into a reputation that opens doors to larger, better-margin projects.

The other mistake I see regularly is assuming that a strong bond replaces strong management. It does not. A bond is a financial backstop, not a project management tool. The contractors who perform best combine solid bonding capacity with rigorous scheduling, pre-vetted subcontractors, and clear contract terms. Workforce management practices, including those covered in resources like this 2026 workforce management guide, reinforce the operational side that bonds cannot cover.

My advice: start building your bonding profile now, not when a specific project demands it. The surety market rewards preparation.

— Rowena

How Constructconnect-rconstructionsolutions helps bonding-ready contractors win more work

Constructconnect-rconstructionsolutions works exclusively in the AEC industry, connecting contractors with pre-vetted talent and sourcing project opportunities that match their bonding capacity and operational strengths.

Contractors who carry performance bonds qualify for a wider range of projects, but only if they have the right team in place to deliver. Constructconnect-rconstructionsolutions’ AEC recruiting services match bonding-qualified contractors with superintendents, project managers, and field staff who have the documented experience sureties look for during underwriting. For contractors ready to pursue larger opportunities, the business opportunity sourcing program connects you with vetted projects that align with your bond capacity and project history. With 30+ years of AEC industry experience, Constructconnect-rconstructionsolutions helps you staff and source with confidence.

FAQ

What is a performance bond in construction?

A performance bond is a three-party financial guarantee between a contractor, a surety company, and a project owner that ensures the contractor completes the project per contract terms. If the contractor defaults, the surety funds completion or compensates the owner up to the bond amount.

When are performance bonds legally required?

The Miller Act requires performance and payment bonds on federal construction contracts over $100,000. State Little Miller Acts impose similar requirements on state-funded public works, with thresholds that vary by state.

How much does a performance bond cost?

Performance bond premiums on commercial projects typically range from 0.75% to 2.5% of the contract price, depending on project risk and the contractor’s credit strength and financial history.

Does a bid bond guarantee a performance bond?

No. A bid bond only guarantees that a contractor will enter the contract if selected. The final performance and payment bonds require separate underwriting and are not automatically issued after a bid bond is accepted.

How does bonding capacity affect a contractor’s business?

Bonding capacity sets a ceiling on the size and number of projects a contractor can pursue simultaneously. Sureties base capacity on audited financials, working capital, and completed project history, so contractors with stronger financial profiles qualify for larger and more projects.