What Is a Subcontractor Performance Bond? 2026 Guide

A subcontractor performance bond is a three-party contractual agreement guaranteeing that a subcontractor will fulfill their project obligations, or the surety company will step in to address the default. The three parties are the subcontractor (principal), the general contractor (obligee), and the surety company. This bond is the industry’s standard mechanism for transferring subcontractor default risk away from the GC and onto a financially rated third party. For construction professionals and project managers, understanding the subcontractor bond definition is not optional. It is a core competency for managing project risk, protecting your bonding capacity, and keeping project schedules intact.

What is a subcontractor performance bond and how does it work?

A performance bond for subcontractors functions as a financial guarantee backed by a licensed surety company. When a subcontractor signs a bonded subcontract, the surety agrees to cover the cost of completing the work or compensating the GC if the subcontractor defaults. This structure shifts the financial exposure from the general contractor to a third party with the resources to respond.

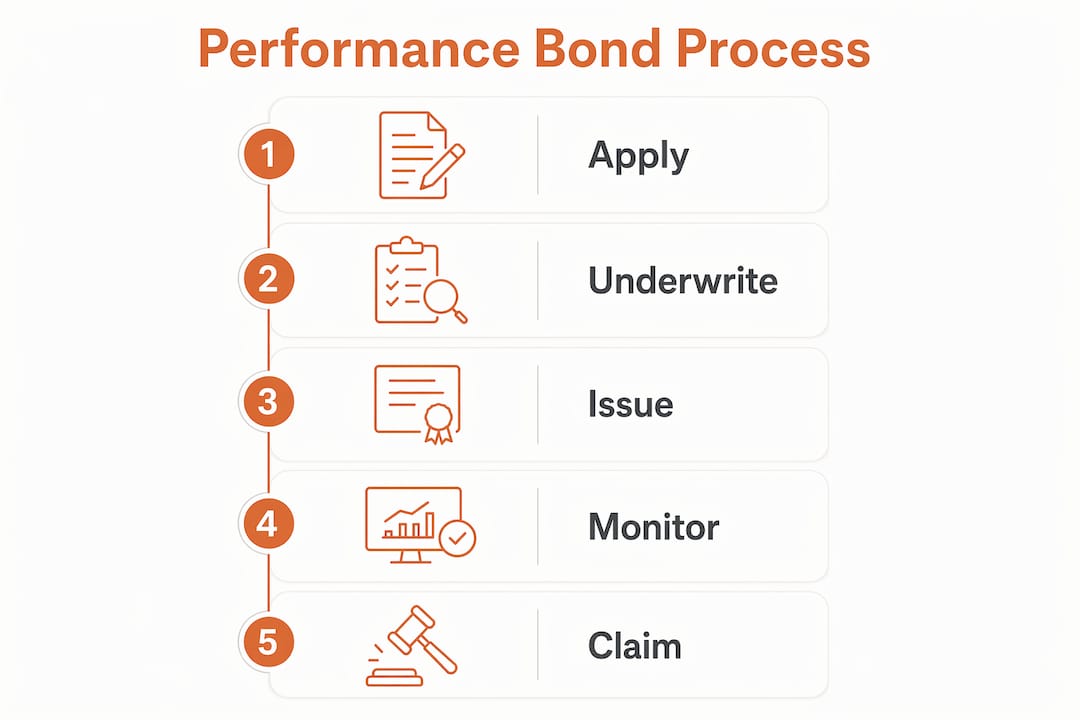

The mechanics follow a clear sequence:

- Bond issuance. The subcontractor applies for a bond from a surety company before or at subcontract execution. The surety reviews the subcontractor’s financials, credit history, and current workload before issuing the bond.

- Default trigger. If the subcontractor fails to perform, abandons the project, or becomes insolvent, the GC declares a default and notifies the surety in writing.

- Surety investigation. The surety investigates the claim to verify the default and assess the GC’s compliance with the subcontract terms.

- Surety remedy. Per the bond terms, surety obligations upon default include completing the remaining work directly, hiring a replacement subcontractor, or reimbursing the GC for documented losses up to the bond penalty amount.

Common scenarios that trigger bond claims include a subcontractor walking off the job mid-project, a specialty trade firm becoming insolvent after receiving early payment, or a subcontractor failing to meet schedule milestones that threaten the prime contract. Subcontractor cash flow gaps between payment request and work completion are a documented driver of default risk, and bonding back subcontractors gives the GC direct leverage to protect against exactly this scenario.

Pro Tip: Always confirm that the surety company is listed on the U.S. Department of the Treasury’s Circular 570, which identifies approved sureties for federal bonds. This applies to both prime and subcontractor bonds.

Benefits and limitations compared to other risk management tools

Performance bonds provide a direct remedy mechanism that retention payments and general liability insurance do not. Understanding where bonds fit in your overall risk management program is what separates a well-structured subcontract from one that leaves you exposed.

What bonds do that other tools cannot

Performance bonds provide immediate financial recourse and risk transfer, unlike retention payments that delay resolution and can disrupt project cash flow for months. Insurance policies cover third-party claims and property damage. They do not cover the cost of completing a subcontractor’s unfinished scope. A performance bond is specifically designed for that gap.

The prequalification value of surety underwriting is a benefit that GCs often underestimate. Surety underwriting involves reviewing subcontractor financials, credit, and current workload before issuing any bond. This means the surety has independently validated the subcontractor’s financial health and capacity before you award the subcontract. You are effectively getting a second opinion on the subcontractor’s ability to perform, at no direct cost to your qualification process.

Requiring bonds also protects the GC’s bonding capacity by reducing the risk that a subcontractor failure cascades into a claim on the prime bond. A subcontractor default that forces the GC to absorb completion costs can impair the GC’s own financial ratios, which sureties monitor closely when renewing prime bonds.

Where bonds fall short

- Bond penalty limits. The bond only covers losses up to the bond amount, which is typically equal to the subcontract value. Consequential damages, such as liquidated damages assessed against the GC by the owner, may not be recoverable.

- Savings clauses. Savings clauses on bonds can affect GC coverage if the GC fails to fulfill its own subcontract obligations. Non-compliance with notice requirements or improper termination procedures can void surety coverage entirely.

- Small subcontract values. For subcontracts under $50,000, the administrative cost of bonding often exceeds the risk benefit. Most GCs set a minimum threshold before requiring bonds.

- Availability for newer firms. Subcontractors with limited financial history or poor credit may not qualify for bonds, which itself is useful information during prequalification but limits your options for that trade.

You can review a subcontractor coverage checklist to see how bonds fit alongside insurance certificates and other compliance documents in a complete risk management framework.

What does a subcontractor performance bond cost?

Typical premium costs for subcontractor performance bonds range from 1% to 3% of the subcontract value, depending on the subcontractor’s credit profile, financial strength, and the complexity of the work. A $500,000 mechanical subcontract, for example, would carry a bond premium between $5,000 and $15,000. That range reflects real differences in underwriting risk.

Key underwriting factors that affect pricing

- Credit score and financial statements. Sureties review two to three years of financial statements, including working capital ratios and net worth. A subcontractor with strong financials qualifies for rates near the 1% floor.

- Current workload and backlog. A subcontractor already at capacity is a higher risk. Sureties assess whether the firm can absorb another project without overextending.

- Subcontract size relative to firm size. A $2 million subcontract awarded to a firm with $1.5 million in annual revenue will face higher premiums or may not qualify at all.

- Specialty trade and project complexity. High-risk trades such as structural steel, mechanical, and electrical work on complex projects carry higher premiums than standard framing or drywall scopes.

- Claims history. Any prior bond claims on the subcontractor’s record will increase premiums significantly or disqualify them from bonding with certain sureties.

Bond costs are typically factored into subcontractor bids, so the GC does not always absorb the premium directly. When you require bonds in your bid documents, subcontractors price the bond cost into their proposal. The net effect is a modest increase in subcontract cost offset by a significant reduction in financial exposure.

Pro Tip: Require subcontractors to submit their bond commitment letter alongside their bid, not after award. This confirms bondability before you commit to the subcontract and avoids the awkward situation of awarding to a subcontractor who cannot actually obtain a bond.

When should general contractors require subcontractor performance bonds?

The decision to require a performance bond is a risk management judgment call, but several clear benchmarks guide that decision in practice.

The National Association of Surety Bond Producers (NASBP) identifies four situations where GCs consistently benefit from requiring subcontractor bonds:

- High-value subcontracts. Most GCs set a threshold between $100,000 and $250,000. Any subcontract above that threshold warrants a bond regardless of the subcontractor’s track record with your firm.

- Specialty or critical-path trades. Mechanical, electrical, plumbing, and structural steel subcontractors sit on the critical path of most projects. A default in any of these trades stops the project. Bonds are standard practice for these scopes.

- New or unproven subcontractors. When you are working with a subcontractor for the first time, the surety’s prequalification process substitutes for the relationship history you do not yet have.

- Early payment situations. When the subcontract structure requires significant upfront payment for materials or mobilization, bonding back subcontractors protects against the risk of a no-show after payment has been released.

Regarding public versus private projects, public projects over $150,000 require prime contractor bonds under the Miller Act, and many public owners flow that requirement down to major subcontractors. Private projects have no statutory mandate, but owners and GCs on large private work routinely require subcontractor bonds as a condition of the subcontract. For contractor licensing requirements that intersect with bonding obligations, the Utah contractor licensing guide provides a useful state-level reference.

| Subcontract scenario | Bond recommended? |

|---|---|

| Subcontract value over $100,000 | Yes, standard practice |

| Critical-path specialty trade | Yes, regardless of value |

| First-time subcontractor relationship | Yes, surety prequalifies |

| Subcontract under $50,000, known sub | Generally no |

| Public project over $150,000 | Yes, often required by law |

Understanding how to qualify subcontractors before project start gives you a structured process for determining when bonds are the right tool and when other prequalification methods are sufficient.

Key takeaways

A subcontractor performance bond is the most direct financial tool a GC has to transfer default risk to a third party while simultaneously validating the subcontractor’s capacity to perform.

| Point | Details |

|---|---|

| Core definition | A three-party agreement where the surety guarantees subcontractor performance or covers default costs. |

| Surety remedies | The surety can complete the work, hire a replacement, or reimburse the GC up to the bond amount. |

| Premium range | Bond premiums typically run 1% to 3% of subcontract value based on credit and risk profile. |

| When to require bonds | Set a threshold at $100,000 or above, and always bond critical-path specialty trades. |

| Savings clause risk | GCs must follow proper notice and termination procedures or risk voiding surety coverage. |

Why I think GCs undervalue the prequalification side of bonding

By Rowena

Most of the conversation around performance bonds focuses on what happens after a default. That framing misses the more immediate value. The surety’s underwriting process is an independent financial audit of your subcontractor, conducted before you sign the subcontract. In 30-plus years of working in the AEC industry, I have seen GCs spend weeks on internal prequalification reviews only to award to a subcontractor who was already overextended. A surety would have caught that.

The uncomfortable reality is that many GCs require bonds on paper but do not enforce the requirement consistently. They waive it for longtime relationships, for low-bid situations where the bond cost feels inconvenient, or when a subcontractor pushes back. That inconsistency is exactly where the exposure lives. The subcontractors most likely to default are often the ones who resist bonding requirements most aggressively.

I also think the savings clause issue is genuinely underappreciated. GCs assume the bond is a safety net they can pull at any time. It is not. If you terminate a subcontractor improperly, fail to provide required notice, or do not follow the cure period specified in the bond form, you can lose your right to make a claim entirely. The bond is only as good as your compliance with the subcontract and bond terms. That means your project managers and contract administrators need to understand bond mechanics, not just your legal team.

The cost argument against requiring bonds rarely holds up under scrutiny. A 1% to 3% premium on a $500,000 subcontract is $5,000 to $15,000. A default on that same subcontract, factoring in completion costs, schedule delays, and potential liquidated damages, can easily reach $150,000 or more. The math is not close.

— Rowena

Source bonded subcontractors with confidence

Finding subcontractors who are both qualified for your project scope and bondable is not always straightforward. Constructconnect-rconstructionsolutions works with construction firms across the AEC industry to source pre-vetted subcontractors and suppliers who meet your bonding, licensing, and performance requirements. With 30-plus years of industry experience and a prorated placement model that means you only pay for successful results, the team connects you with partners who can actually perform. Explore AEC recruiting services to see how the sourcing process works, or visit R. Construction Solutions for a full overview of talent and subcontractor sourcing solutions tailored to your project needs.

FAQ

What is a subcontractor performance bond in simple terms?

A subcontractor performance bond is a guarantee from a surety company that a subcontractor will complete their contracted work. If the subcontractor defaults, the surety steps in to complete the work, hire a replacement, or compensate the general contractor for losses.

How does a performance bond differ from subcontractor insurance?

A performance bond covers the cost of completing unfinished work when a subcontractor defaults, while insurance covers third-party claims and property damage. The two tools address different risks and are typically required together, not as alternatives.

What are typical subcontractor bond requirements for public projects?

Under the Miller Act, federal public projects over $150,000 require prime contractor performance and payment bonds. Many public owners extend this requirement to major subcontractors, and most state and local public projects follow similar thresholds.

Who pays for a subcontractor performance bond?

The subcontractor applies for and pays the bond premium, which typically runs 1% to 3% of the subcontract value. In practice, subcontractors factor this cost into their bid price, so the expense is often passed through to the project budget.

Can a GC lose bond coverage even after requiring a bond?

Yes. Savings clauses in bond forms mean that if the GC fails to follow proper termination procedures, provide required notice, or fulfill its own subcontract obligations, the surety can deny the claim. Proper contract administration is required to preserve bond rights.